Laos in Translation

How Russia found a bank in Laos, and what it tells us about the next generation of sanctions evasion

Good morning! This is my first piece under Evidence of Absence, my little corner of the internet where I hope to make some of the more opaque parts of illicit finance a little easier to understand.

Quickly, a little about me. Over the last few years, I’ve spent an unreasonable amount of time tracing payment chains, sanctions evasion networks, and financial infrastructure across jurisdictions. Before that, I spent nearly a decade in the US Intelligence Community doing this kind of work with classified data. Now I do it with public data and a lot more patience. Increasingly, I think the findings are often better.

The name Evidence of Absence comes from a Carl Sagan line I’ve always appreciated: “absence of evidence is not evidence of absence.” In intelligence analysis, the absence has always been the point where I’ve been most intrigued. Sagan’s line also makes an appearance in a scene in The Boondocks, where it is tied to a Rumsfeld response to an interviewer, which felt reason enough to keep it.

The full report is linked at the bottom.

But first: Laos.

Here is what I think happened.

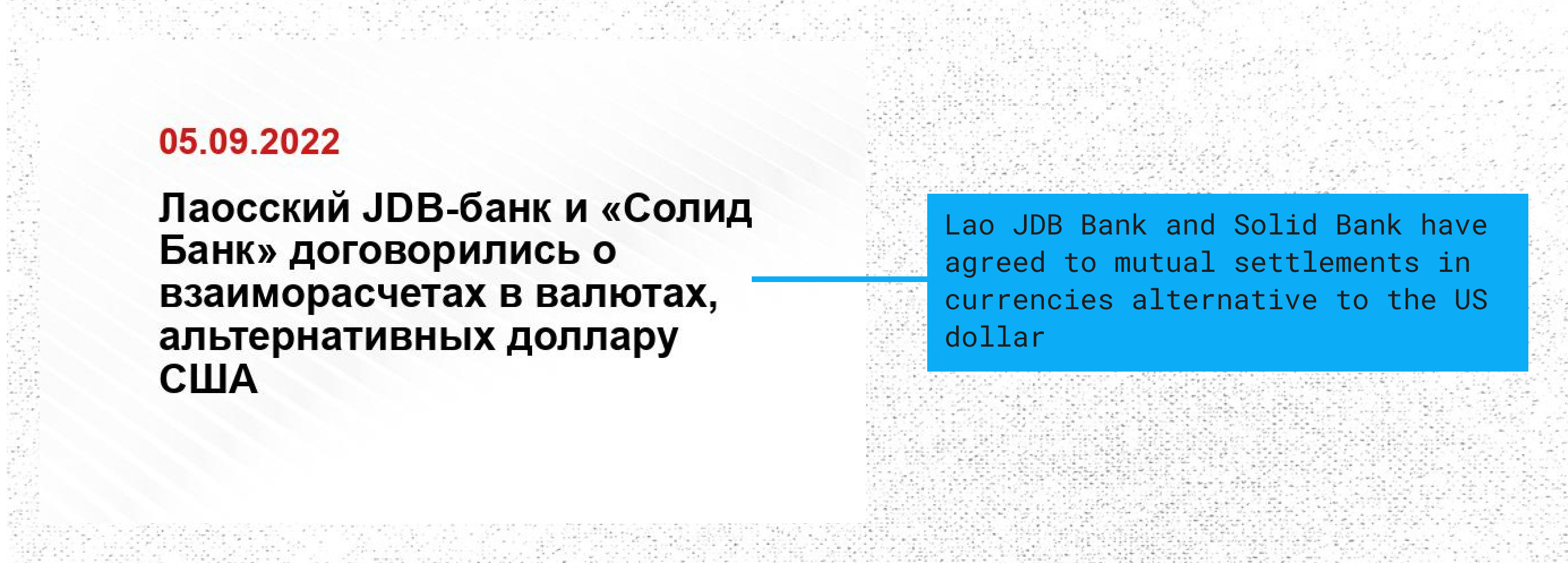

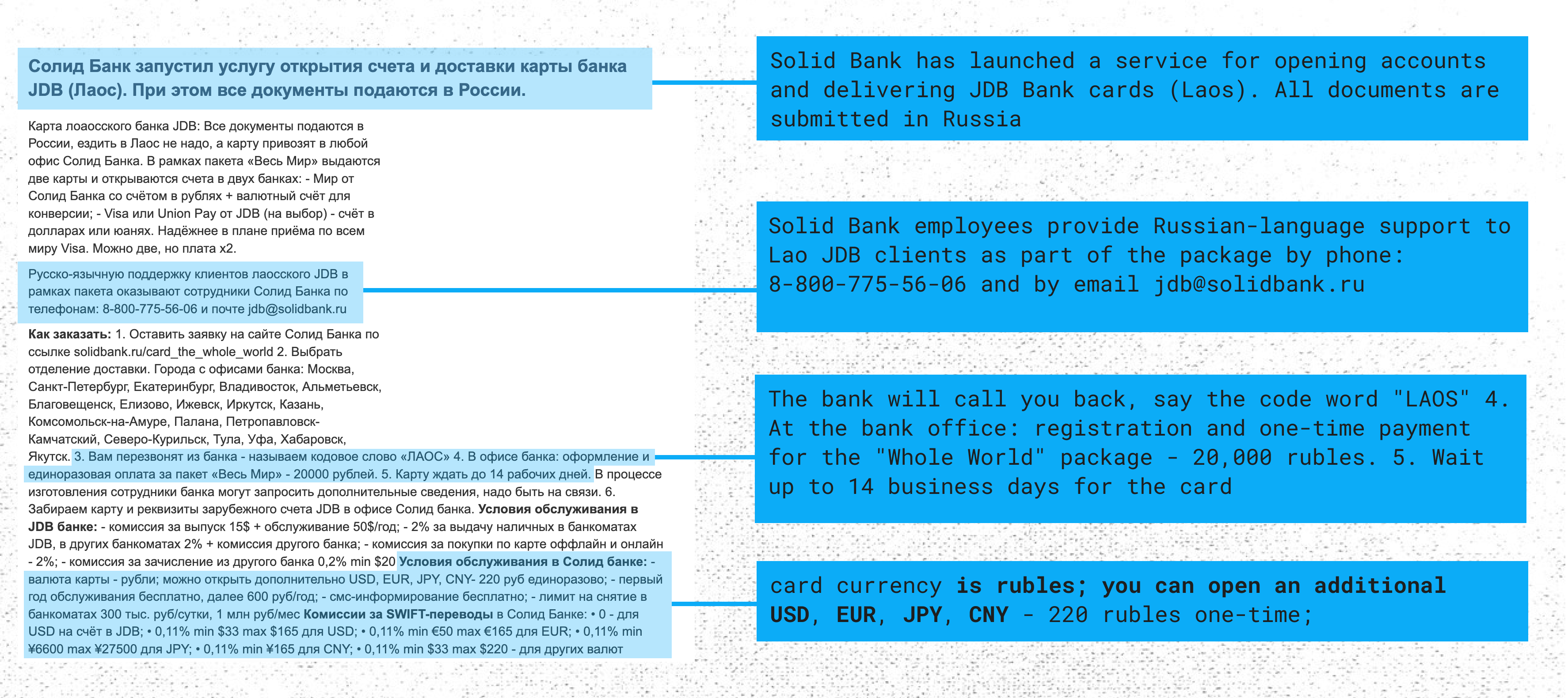

A Russian bank in Vladivostok, sanctioned by the UK in October 2025 for helping Russia finance its war, started advertising to its customers that they could open a bank account in Laos.12 Quite literally: send us your documents, we will process them in Russia, and we will mail you a Visa card from a Laotian bank.3 The service costs RUB 2,500 plus 0.25% per transaction. It is marketed as a retail banking product.

The Laotian bank is called Joint Development Bank, known as JDB, and is the fourth-largest bank in Laos, with $1.5bn in assets, Big Four audit support, and a Visa card program. In so many cases we talk about shell companies or single-purpose banks, but this is a real bank with real customers. In fact, the bank was founded with state-backing in 1989.

As of 14 May 2026, JDB is also an EU-designated entity, named in the 20th Russia sanctions package as a third-country institution that “helped circumvent sanctions or was linked to Russian financial infrastructure.”4

JDB has not been more widely designated, as of 19 May 2026. And the vulnerabilities discussed here are not necessarily ones that sanctions alone can solve. That is what I want to talk about.

Why Laos?

When you think about Russian sanctions evasion, you probably think about the UAE. Fair enough. Lots of people do, myself included. The UAE is where the documented networks are, where the shell companies are found, & where the first wave of post-2022 workarounds found a home. It’s also where my first post-government piece focused when I identified that Russian banks were swapping gold bars for foreign currencies.

But the UAE has a bit of a structural problem: its banks still have direct correspondents in the US and Europe. When a UAE company sends a SWIFT payment, that payment passes through a bank that a Western regulator can see, and potentially stop. Additionally, the UAE has a requirement to at-least appear compliant. This is because the UAE is important for the rest of the World, not just Russia.

Laos does not have this problem to the same extent. It’s economy is much smaller and more isolated.

JDB holds no direct US correspondent. No European correspondent. No major Western banks in its payment chain. When foreign money enters JDB, it exits exclusively through Bangkok Bank or KasikornBank in Thailand, two large Thai institutions handling volumes that dwarf anything a Russia-Laos corridor would generate. By the time a payment arrives at either Thai bank, the Russian origin has passed through two jurisdictional hops and a currency conversion. Without active cooperation from Thai regulators, it is mostly invisible to Western oversight.

As I’ve seen in other investigations in the region, the introduction of distance in the correspondent chain is by design.

A brief word on correspondent banking

(This is an area that I’ve been trying to sound the alarm on for years. The house is on fire. Hang tight with me for two minutes.)

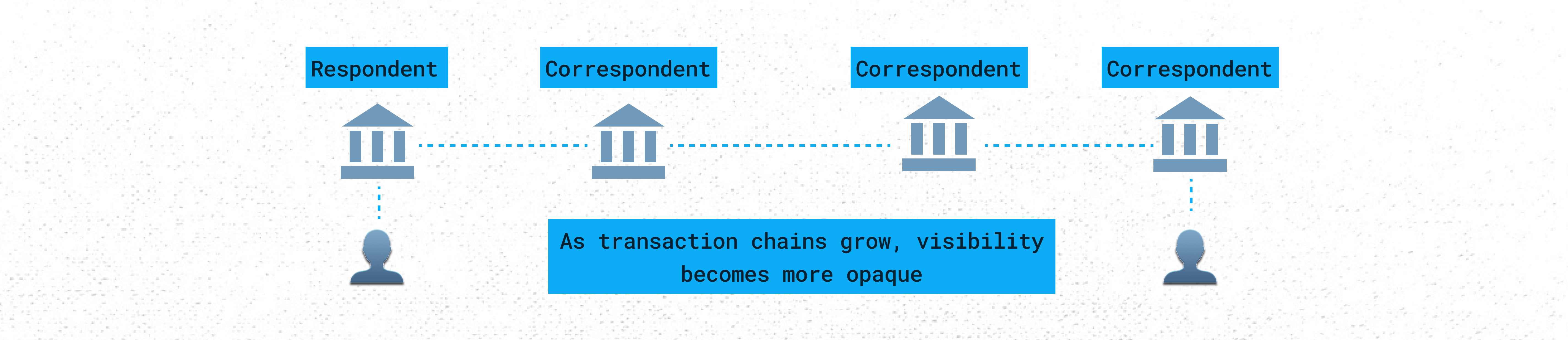

Most people picture international money transfers like sending an email: you press send, it arrives. The reality is closer to a postal system. Your letter passes through several branch offices before it reaches its destination, and each one stamps it and logs it before passing it to the next.

Banks do not maintain direct relationships with every other bank in the world. There are so many of them and this would be impossible. What they do instead is maintain relationships with a smaller number of larger banks that have global reach. Your bank might not have a branch in Laos. Maybe a larger institution does? So when money needs to move from London to Vientiane, it travels through a chain: your bank tells the large bank to pay, the larger bank finds a bank in the relevant country and instructs payment, that bank credits the recipient’s account. Each of those intermediate banks is called a correspondent.

SWIFT is the messaging system that carries those instructions. It is not a bank. It does not hold money. It is the international postal system for payment orders, a standardized way for banks to say to each other: pay this person, this amount, from this account. When Russia was cut off from SWIFT in 2022, this is what it lost: the ability to send those instructions internationally. Russian banks could still move money domestically. They just could not tell a foreign bank to do anything.

Here is the part that matters for everything that follows.

Every correspondent bank in a payment chain has legal obligations. It is supposed to screen the transaction, check the parties against sanctions lists, and flag anything suspicious. If a US bank is anywhere in the chain, US law applies. If a European bank is anywhere in the chain, European law applies. This is why the US dollar being the world’s reserve currency gives Washington such extraordinary reach over international finance: virtually every dollar transaction touches a US correspondent somewhere.

The evasion strategy, therefore, is straightforward in theory and slightly harder in practice: design a payment chain where no US bank and no European bank can track where the money originated from. As long as money originates outside of Russia and moves internationally then it will be processed as normal. It just needs to originate from jurisdictions where the oversight is thinner, the regulators are underfunded, Russia exerts influence, and the political appetite to investigate Russian money is limited.

JDB has no direct US correspondent and no direct European correspondent. That sentence is doing a lot of work in this story.

The numbers that don’t really add up

I also wanted to highlight something from JDB’s financial profile, because this is the part that moved this from “interesting” to “worth looking closely.”

| Metric | 2024 | 2023 | 2022 | 2021 |

| ---------------------- | ---------- | ---- | ---- | ---- |

| Net interest revenue | $21M | $16M | $17M | $13M |

| Other operating income | **$47M** | $34M | $20M | $17M |

| Profit margin | **61.97%** | - | - | - |Other Operating Income is what banks earn from things like fees, FX conversions, and correspondent services: the transactional side of the business. Net Interest Revenue is what banks earn from lending, which is the actual business of being a bank.

At JDB, the fee side is more than double the lending side. On a $1.5bn asset base. With a 61.97% profit margin.

I have spent an unreasonable amount of time looking at bank financials. What I can say is that margin is not a conventional or consistent profit spread of a commercial bank serving Laotian retail customers. The data is consistent with a bank generating substantial revenue from processing payments on behalf of third parties.

Considering this temporally makes it worse. Other Operating Income went from $17M in 2021 to $47M in 2024, a 176% increase over three years and outpaces Net Interest Revenue. That growth starts in 2022. You do not need me to tell you what else happened in 2022.

How the money moves

The Russian bank is called Solid Bank, headquartered in Vladivostok.5 It is 46.80% owned by a Japanese holding company called HS Holdings, which also owns banks in Mongolia and Kyrgyzstan. The remaining majority is controlled by a Russian family through two entities. Alongside Solid Bank, HS Holdings’ banking portfolio includes Khan Bank in Mongolia and Kyrgyz Commerz Bank in Kyrgyzstan.

Solid Bank’s own press materials explicitly describe the JDB partnership as being about “mutual settlements in currencies alternative to the US dollar.” The advertised purpose is to move money outside the dollar system.

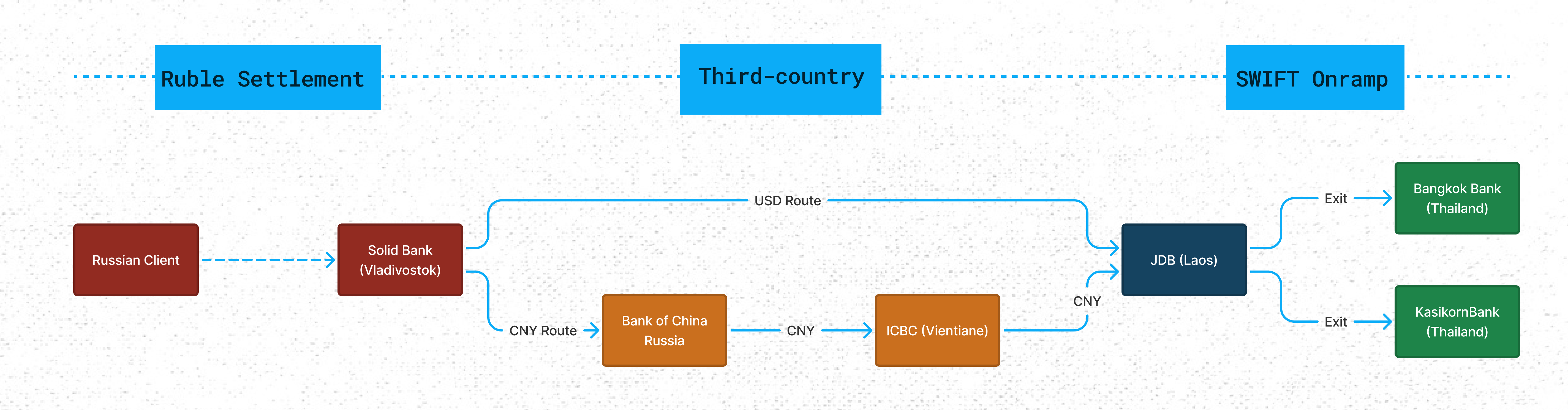

There could be at least two main routes:

The CNY route: Russian client → Solid Bank → Bank of China Russia → ICBC Vientiane → JDB. No US or European institution touches it directly.

The USD route: Funds move into JDB’s settlement account, then onramp through Bangkok Bank or KasikornBank, who maintain the USD access. The Russian origin is not visible to Thai bank by the time the payment arrives.

There is also a domestic leg that never appears on SWIFT at all. In previous Russian evasion networks I have researched, domestic ruble settlement happened through securities-based products, keeping ruble settlement off international messaging systems. In this architecture, the equivalent is likely SPFS / СПФС (System for Transfer of Financial Messages / Система передачи финансовых сообщений), Russia’s domestic financial messaging system. The Central Bank of Russia stopped publishing its membership list, so direct confirmation is not available from open sources. What is confirmed is that the EU designated JDB as linked to “Russian financial infrastructure.” SPFS connectivity is precisely what that this phrase appears to describe.

What this could mean

The EU has already acted. Any EU-regulated institution is now prohibited from transacting with JDB. But, due to the complexities of correspondent banking, do they even know?

Solid Bank, the Russian bank that built and advertised this corridor, is UK-designated. Its minority owner is a Japanese-based holding company with other banks in its portfolio. Specifically, banks in jurisdictions that Russia is known to have used to access Western financial systems through similar means.

JDB’s beneficial ownership runs through a Laotian conglomerate called Simeuang Group, which acquired the bank in 2012. The bank operates in a jurisdiction that FATF placed on its grey list in February 2025 and ranks seventh worst globally on the 2025 Basel AML Index, in the company of Myanmar, Haiti, and Venezuela.67

To be abundantly clear, I am not saying JDB is knowingly complicit. That is a question for investigators with regulatory oversight. What I am saying is that its financial profile, its correspondent network, its partnership with a UK-sanctioned Russian bank, activity adjacent to other prominent evasion corridors, and its income trajectory since 2022 together constitute a set of facts that warrant a serious look.

Russia replacing SWIFT with SPFS isn’t likely to happen. Definitely not at scale, not in this reality, and that’s something that I feel confident in saying. But that’s almost beside the point. The architecture described in this piece doesn’t need SPFS to win. It just needs enough JDBs in just enough jurisdictions where the oversight is thin, the volumes are unremarkable, and nobody is asking questions. One bank in Laos is an interesting story. twenty banks in twenty countries looks more like infrastructure. I believe that we are somewhere between those two points right now, and the distance is closing faster than the regulatory response.

The detailed version of this post, as a standalone piece, including SWIFT correspondent tables, corporate ownership data, financial profiles, payment chain diagrams, and more details is linked below. It is freely available, just please drop a request.

Zachary Tvarozna is formerly of the US Intelligence Community and does his best to maintain Evidence of Absence alongside other engagements. He works with governments, the private sector, and investigative media partners on sanctions evasion and financial crime. His work has been cited in Bloomberg, The Kyiv Post, and The Hill. He is also an avid cyclist and fan of punk rock.

If this is useful to you, please do subscribe and reach out. Future investigations will come here first.

https://www.opensanctions.org/entities/NK-Z3exaBPY5AM98Joh736oSg/

https://vladivostok.sm.news/laosskij-jdb-bank-i-solid-bank-dogovorilis-o-vzaimoraschetax-v-valyutax-alternativnyx-dollaru-ssha-79351-u3t5/

https://sia.ru/?section=484&action=show_news&id=439174

https://eur-lex.europa.eu/eli/dec/2026/508/oj

SWIFT: SLDBRUMMXXX, INN: 4101011782

https://www.fatf-gafi.org/en/countries/detail/Lao-People-s-Democratic-Republic.html

https://index.baselgovernance.org/ranking